The Shift to Digital-First Banking Architectures

Modern digital only services manage multiple current accounts by offering unified dashboards, sub-account spaces (such as Revolut Pockets or Monzo Pots), instant virtual cards, and automated salary sorting. These fintech platforms allow individuals and freelancers to separate expenses and currencies without brick-and-mortar branch visits. Integrating these services with browser isolation platforms like Send.win ensures secure, simultaneous access to all your banking dashboards.

The traditional banking model, built around physical branches and legacy mainframe systems, is increasingly ill-suited for modern financial management. For decades, opening a secondary checking or savings account required scheduled appointments, manual paperwork, and high monthly fees. Today, neobanks and digital-first financial services have revolutionized this space. They offer flexible, multi-account structures that allow users to create, configure, and fund separate digital wallets in seconds. For individuals seeking to optimize their personal budgeting, and freelancers looking to keep business and personal finances separate, these services are essential tools.

However, as users open multiple accounts across different digital banks to maximize interest rates or access specialized features, they encounter a new challenge: dashboard sprawl. Juggling active sessions across Revolut, Monzo, Wise, and traditional banks in a standard web browser leads to constant security verification loops and session timeouts. In this comparison guide, we will analyze the top digital banking platforms, outline the best budgeting frameworks, explore the security challenges of managing multiple financial dashboards, and demonstrate how advanced session isolation simplifies your digital banking workflow.

Why Modern Budgets Require Multiple Current Accounts

Historically, consumers managed their money using a single checking account and a single savings account. Today, financial advisors recommend utilizing a multi-account structure to automate budgeting and protect capital. The benefits of this approach include:

- Automated Expense Segmentation: Dedicated accounts for fixed bills, variable spending, and emergency savings prevent you from accidentally spending money reserved for rent or utility bills.

- Enhanced Fraud Protection: By keeping the majority of your cash in an offline savings pocket and linking only a small amount to your daily debit card, you limit your financial exposure if your card details are stolen.

- Seamless Business Operations: Freelancers, contractors, and e-commerce merchants can isolate business income from personal spending, making tax preparation and expense tracking straightforward.

To implement this setup without administrative headache, users are turning to digital-only banks that support instant sub-account creation and automated transfers.

Top Digital Banking Platforms Compared

Several neobanks and digital payment services offer excellent multi-account functionality. Here is how the top services compare in 2026.

1. Revolut

Revolut is a global leader in neobanking, offering highly flexible multi-account features. Within the main Revolut application, users can create “Pockets” — dedicated sub-accounts designed to hold money for specific bills or savings goals. Users can link virtual debit cards to specific pockets, ensuring that transactions are routed from the correct balance. Revolut also supports multi-currency accounts, allowing users to hold and exchange over 30 currencies. Pricing tiers range from a free basic plan to premium tiers like Pro ($9.99/mo) and Metal ($13.99/mo).

2. Monzo

Monzo is a dominant force in the UK digital banking sector. Its core feature is the “Pots” system, which allows users to separate their money from their main balance. Monzo’s “Salary Sorter” automatically distributes incoming paychecks across savings pots, bills pots, and spending balances the moment they arrive. Monzo also offers shared pots for joint expenses and dedicated business banking profiles with built-in invoicing tools. Plans range from free to £15/month for the Premium tier.

3. Wise

Wise is the premier platform for managing international accounts. Rather than offering traditional banking services, Wise provides multi-currency accounts that allow users to hold and convert over 40 currencies. Wise also gives users local account details (such as IBANs and routing numbers) for the US, UK, Europe, Australia, and Canada. This allows freelancers to receive payments like a local resident. Wise is free to set up, charging small, transparent conversion fees when converting currency.

4. N26

N26 is a popular European digital bank that operates via a full German banking license. It features “Spaces” — sub-accounts that can be created in seconds for budgeting and savings targets. N26’s “Shared Spaces” feature allows premium users to invite friends or colleagues to pool funds in a shared sub-account, making it a great solution for shared household bills. Paid plans start at €4.90/month.

A Strategic 4-Account Framework for Personal Budgets

To manage multiple current accounts effectively, financial planners suggest setting up the following four-part structure:

- The Income Hub: The primary account where your direct deposit paycheck lands. No spending occurs here; money is immediately distributed to the other accounts on payday.

- The Fixed Bills Account: A dedicated account that holds funds reserved for fixed expenses (rent, utilities, insurance, loan payments). All auto-draft bills should link to this account.

- The Daily Spending Balance: The account you use for variable day-to-day spending (groceries, dining, entertainment). Link your primary debit card to this balance.

- The Emergency Fund: A high-yield savings vault containing 3 to 6 months of expenses, kept separate from daily balances to prevent impulse withdrawals.

How Wise Redefines Multi-Currency Account Management

For individuals and international freelancers, Wise has transformed the multi-account landscape by focusing heavily on cross-border transactions and real-time exchange rates. While standard digital-only banks charge hidden markups on international currency conversions, Wise utilizes the mid-market exchange rate and charges a small, transparent fee disclosed upfront. This is particularly valuable for professionals receiving payments in USD, EUR, GBP, and AUD. Wise issues real, local bank routing and account numbers for these jurisdictions, effectively giving you localized banking presence without requiring residency in those countries.

Operational flexibility is further enhanced by Wise’s business accounts. Companies can run batch payments to send funds to up to 1,000 recipients worldwide in a single click. From a regulatory perspective, it is important to note that Wise operates as an Authorized Electronic Money Institution (EMI) rather than a licensed bank in many regions. This means that while funds are not covered by traditional government deposit insurance (like the FDIC in the US or FSCS in the UK), they are protected through safeguarding rules. Under safeguarding, Wise is legally required to keep 100% of customer funds in low-risk asset accounts at major financial institutions separate from its own corporate funds, ensuring customer capital is protected even if the platform experiences insolvency.

Developing a Unified Financial Operation for Freelancers

Freelancers and independent contractors face the unique challenge of managing unpredictable income streams while maintaining clean business-and-personal financial boundaries. To address this, a structured multi-account operation is essential. Freelancers should establish a primary Business Checking account to receive all client payouts. Next, a secondary “Tax Reserve” sub-account should be configured. By setting up automated transfer rules, freelancers can direct exactly 30% of every incoming client invoice into their Tax Reserve pocket immediately, preventing tax-time cash flow shortages.

Operating costs, including software subscriptions, hardware amortization, and professional services, should be paid from a dedicated “Operating Expenses” sub-account linked to a unique virtual debit card. This ensures that business deductions are automatically categorized and easily exportable for tax filing. Finally, the owner’s salary, or “draw,” should be paid via a scheduled monthly transfer from the business checking account to a completely separate personal checking account. This clean separation protects the business owner’s personal assets and ensures a disciplined approach to budgeting.

Regulatory Compliance and Financial Safety in Digital Banking

Operating multiple digital banking accounts requires a solid understanding of the regulatory safeguards that protect your money. In the United Kingdom, licensed neobanks like Monzo and Starling Bank are fully regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA), meaning customer deposits are protected by the Financial Services Compensation Scheme (FSCS) up to £85,000 per person. In the United States, digital-first banking apps like Chime partner with traditional FDIC-insured institutions (such as The Bancorp Bank or Stride Bank) to provide coverage up to $250,000.

For businesses and high-net-worth individuals, managing cash balances that exceed these safety limits requires a multi-bank diversification strategy. Rather than keeping all capital in a single platform, accounts should be spread across different banking licenses. This diversification also mitigates “single-point-of-failure” risks. If a neobank’s server network goes offline or experiences a temporary freeze due to fraud sweeps, having secondary accounts active at a different digital bank ensures that your business can continue to process payroll and execute client payments without interruption.

Managing Multiple Banking Portals Securely

While digital banking platforms simplify money management, accessing multiple financial dashboards introduces distinct operational and security challenges. When you attempt to manage different platforms in a standard web browser, you face session conflicts. For example, if you open multiple accounts on the same banking platform using different tabs, the browser’s shared cookie jar can cause session errors or log you out. To prevent this, users need a dedicated cookie management tool that isolates session data per tab.

Additionally, users who configure multiple browser profiles to manage different bank logins find that local browser setups are resource-heavy. Each profile runs a separate browser instance, consuming significant RAM. A cleaner option is to use a structured chrome multi account environment that streamlines session management. This is highly relevant when managing sensitive financial portals that enforce short session timeouts and strict multi-factor authentication checks.

For business owners and freelancers, this separation is a security requirement. When accessing a business browser for ads management dashboard or a client advertising console, you must ensure that your banking sessions are isolated to prevent cross-site scripting attacks. Similarly, contractors managing multiple amazon accounts alongside multiple business bank accounts must prevent their digital footprints from merging, protecting their retail stores from automated fraud detection sweeps.

Digital Banking Platform Comparison

The table below summarizes the key operational differences between the leading digital-only banking and payment services in 2026.

| Banking Service | Primary License | Sub-Account Architecture | Multi-Currency Support | Business Integration | Monthly Base Price |

|---|---|---|---|---|---|

| Revolut | European Bank License | Unlimited “Pockets” | Very High (30+ Currencies) | Revolut Business supported | Free (Paid plans from $2.99) |

| Monzo | UK Bank License | Unlimited “Pots” | Low (FX via partners) | Monzo Business supported | Free (Paid plans from £5) |

| Wise | E-Money Institution | Multi-currency balances | Extremely High (40+ Currencies) | Wise Business with API | Free to set up |

| N26 | German Bank License | Up to 10 “Spaces” | Low (EUR base) | N26 Business supported | Free (Paid plans from €4.90) |

| Starling Bank | UK Bank License | “Spending Spaces” | Moderate (GBP/EUR) | Starling Business Toolkit | Free |

| Chime | US Partner Banks | Savings Account Vault | Low (USD only) | Not supported | Free |

Automation and API Integration in Fintech Banking

For developers, technology startups, and scaling agencies, manually logging in to extract statements and sync ledgers is highly inefficient. Open Banking APIs and developer webhooks allow users to automate these processes securely. Many digital-first financial services, such as Wise Business and Revolut Business, offer public APIs that enable users to programmatically trigger payouts, check exchange rates, and fetch monthly statement data in real-time.

Firms can utilize Send.win’s local Automation API, available on the Pro plan, to integrate these web portals into their existing software workflows. By using developer tools like Puppeteer, Playwright, or Selenium against the Send.win profile interface, you can automate financial reporting and data export tasks without compromising credentials. This is highly useful for automating daily invoice reconciliations or client reporting dashboards, allowing you to run background operations across multiple bank dashboards safely and cost-effectively.

Seamless Financial Workflows with Send.win

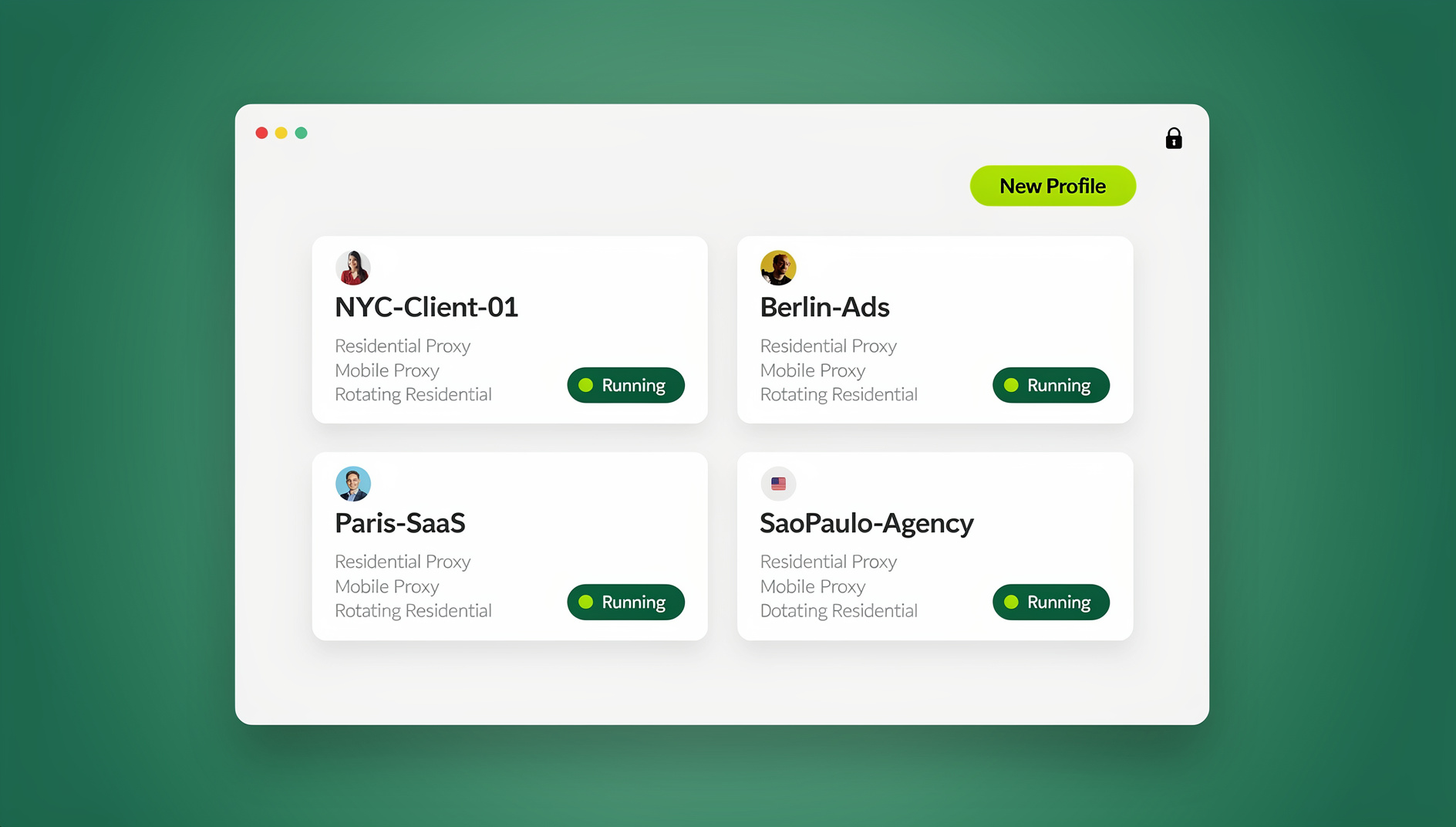

Financial professionals and business owners can streamline their multi-account banking workflows by utilizing Send.win. Send.win is a specialized multi-login browser that isolates session cookies and hardware fingerprints per profile, preventing session conflicts and logouts. Send.win supports two flexible operational modes:

- Sendwin Browser: A native desktop application for Windows, macOS, and Linux that runs isolated browser profiles locally. This provides maximum speed, security, and hardware compatibility.

- Cloud Browser Sessions: A zero-install solution that runs browser profiles in secure cloud environments, allowing you to access all your banking dashboards safely from any workstation or mobile device.

By deploying a dedicated Send.win profile for each banking service, you can monitor all your financial accounts simultaneously. The Pro plan, priced at $9.99/month ($6.99/month billed annually), includes the local Automation API, enabling advanced users to automate financial reporting using Puppeteer or Playwright. Send.win offers a 30-day free trial with no credit card required, allowing you to test the platform’s advanced security capabilities risk-free.

🏆 Send.win Verdict

Managing multiple neobank accounts is essential for modern budgeting, but it often leads to severe dashboard sprawl and session conflicts. Send.win solves this by isolating each banking session inside the Sendwin Browser desktop client or secure cloud browser sessions, ensuring that your accounts remain logged in, separate, and secure from cross-site vulnerabilities.

Try Send.win free today — Start your 30-day free trial now to unify your financial portals and simplify your multi-account management.

Frequently Asked Questions

How do digital only services manage multiple current accounts?

Digital only services manage multiple current accounts by allowing users to create virtual sub-accounts (such as Monzo Pots or Revolut Pockets) instantly within a single app. These sub-accounts can have dedicated virtual cards and automated rules to split income and pay bills automatically.

Are digital-only bank accounts safe?

Yes. Registered digital-only banks hold full banking licenses and offer the same government deposit protections as traditional banks. In the UK, the FSCS covers deposits up to £85,000 per person, while in the US, the FDIC covers deposits up to $250,000 through partner banks.

Can I have multiple current accounts with different digital banks?

Yes, you can hold accounts across as many digital banks as you want. Many users combine Revolut for daily spending, Monzo for automated budgeting, and Wise for handling international currencies to build their ideal financial stack.

What is the difference between a neobank and an e-money institution?

A neobank holds a full banking license, allowing it to offer overdrafts, loans, and government-backed deposit insurance. An e-money institution (like Wise) can hold and transfer funds but cannot lend money or offer government deposit insurance directly, though they must keep customer funds safeguarded in separate trust accounts.

How do automated salary sorters work?

Automated salary sorters detect when a direct deposit paycheck lands in your account and automatically split the funds based on percentages or amounts you define, directing money into separate savings pots or bill pockets instantly.

Do digital bank accounts affect my credit score?

No, opening a basic current account (checking account) without an overdraft facility does not affect your credit score. The bank may perform a “soft search” to verify your identity, which is visible on your report but does not impact your credit rating.

How does Send.win secure my online banking sessions?

Send.win secures your banking sessions by sandboxing each browser profile. This keeps cookies, cache, and local storage isolated, preventing other sites from tracking your session data and protecting you from cross-site scripting vulnerabilities.